Why Legal Tender?

While conceptually all cryptocurrencies can be exchanged for legal tender, and a handful are even loosely linked to a national currency, none actually are legal tender. By contrast the Quint functions like a deed to certify the bearer’s whole or partial ownership of a specified amount of real, nationally-issued money, held on deposit, payable to the token bearer on demand. In this respect, it acts like the U.S. Gold & Silver Certificates of yesteryear once did. This Quintric promise to pay rests firmly on 100% vaulted, insured, legal tender in tangible specie form—not on the the digital promise to pay on a virtual currency launched on a fiat paper system layered over a "print more when you need it" monetary policy.

A. Not Taxable Property

Legal tender is a special kind of personal property, constituting government authorized coins, currencies and bank notes legally approved to serve as a medium of exchange and for payment of public and private obligations. When used as a medium of exchange, legal tender is expressly exempt from taxation, per se. However, typical cryptocurrencies are not treated this way. On March 26, 2014 The United States Internal Revenue Service (“IRS”) released Notice 2014-21, IRS Virtual Currency Guidance. Notice 2014-21 first reaffirms that virtual currencies, such as Bitcoin do “not have legal tender status in any jurisdiction,” and then goes on to state that “[i]f the fair market value of property received in exchange for virtual currency exceeds the taxpayer’s adjusted basis of the virtual currency, the taxpayer has a taxable gain.” In other words, without legal tender status, the “means of the exchange” is regarded as a separate part of the trade and is also measured in transactions, regardless of whether the trading of other property might otherwise be tax neutral. A week after the IRS notice, it was no joke that on April Fool’s day of 2014, in an article and video interview published in Yahoo Finance, CNBC contributor Gina Sanchez lamented:

"It's a terrible thing," says Sanchez of Bitcoin's IRS categorization. "This is already a really negative story, in my opinion. What this says is every time you make a transaction, you basically have to keep track of your capital gains — every transaction."

She added in the interview portion, “That’s ridiculous. If you are using it to buy coffee, that’s ridiculous.”10 While property is often afforded preferential treatment in terms of long-term capital gains tax rates, short-term gains and losses are generally not granted these lower rates. Daily market value fluctuations in an actively used cryptocurrency can create an accounting nightmare, even if tax treatment itself is not adverse for a specific user. The writing is on the wall for virtual currency users. Since the release of that 2014 notice: (1) the federal judiciary has authorized the IRS to serve John Doe summons on Coinbase Inc., seeking information about U.S. taxpayers who conducted transactions in convertible virtual currency; (2) the U.S. Commodity Futures Trading Commission (CFTC) has declared that Bitcoin (like other virtual currencies) falls within the broad definition of a “commodity”; and (3) U.S. state banking regulators have signaled that financial regulatory requirements should extend to activity involving bitcoin and other virtual currencies.

Legally, transactions employing anything other than legal tender as a medium of exchange are treated as barter transactions, so what was previously a simple purchase of a good or service now requires a income gain or loss analysis under § 1001 of the Internal Revenue Code, which reads in part as follows:

(a) Computation of gain or loss.—The gain from the sale or other disposition of property shall be the excess of the amount realized therefrom over the adjusted basis …

(b) Amount realized.—The amount realized from the sale or other disposition of property shall be the sum of any money received plus the fair market value of the property (other than money) received. …

While daunting to contemplate compliance with these provisions, they nevertheless constitute the state of the law for U.S. citizens engaged in the use of cryptocurrencies.

B. Authorized Payment of Debts

In stark contrast to the bookkeeping obstacles and complexities of barter transactions, which require tracking the taxpayer’s tax basis in the non-legal-tender medium of exchange, federal law simply provides:

United States coins and currency (including Federal reserve notes and circulating notes of Federal reserve banks and national banks) are legal tender for all debts, public charges, taxes, and dues.11

U.S. precious metal minted coinage is expressly included within the definition of legal tender.12 Moreover, recent years have witnessed a growing trend among the several States to adopt legislation expressly recognizing U.S. minted precious metal coin as legal tender. Such action reinforces existing federal law while also constituting an exercise of each State’s reserved right under the United States Constitution which provides that “No State shall ... make anything but gold and silver coin a tender in payment of debts.”13

For example, in 2011 the Utah legislature adopted the Specie Legal Tender Act by which it became the first State in more than a century to expressly recognize gold and silver coin as a legally authorized medium of exchange and to eliminate state capital gains taxes on the same.14 Amendments adopted in 2012 dealt with how to calculate and remit sales taxes on purchases consummated in specie legal tender. In 2014, Oklahoma adopted similar specie legal tender legislation.15 That same year Texas and Louisiana enacted elements of the foregoing, and Texas even authorized a state-run, gold repository. In 2017, Arizona likewise recognized specie legal tender and abolished state capital gains taxes on gold and silver.16 At present, five states have laws expressly recognizing gold and silver coin as legal tender, including two statutes that date from the 19th century.17

The U.S. Supreme Court recognized in Lane County v. Oregon, 74 U. S. 71 (1868) that in the performance of its “essential functions” a State possesses broad powers to specify acceptable tender for the payment of taxes:

If, therefore, the condition of any State, in the judgment of its legislature, requires the collection of taxes in kind, that is to say, by the delivery to the proper officers of a certain proportion of products, or in gold and silver bullion, or in gold and silver coin, it is not easy to see upon what principle the national legislature can interfere with the exercise, to that end, of this power, original in the States, and never as yet surrendered.

Whether paying for goods, services or taxes, specie legal tender is an authorized medium of exchange.

C. Allows for Choice in Currency

Functionally, the United States today has five distinct legal tender currency standards—Gold, Silver, Platinum, and base metal coins, as well as the Federal Reserve Note ("paper") dollar,18 together with its derivatives. Although the U.S. Secretary of the Treasury is "to maintain the equal purchasing power of each kind of United States currency",19 he has largely neglected to do so. As a result the purchasing power of the various U.S. currencies currently in circulation, particularly that of specie legal tender in contrast to that of the fiat paper currency, has increasingly diverged over the past several decades, which creates hazards as well as opportunities for individuals, businesses, and governmental entities alike. Even so, according to the federal courts, legally “a dollar is a dollar regardless of the physical embodiment of the currency.”20 In the real world, however, the kind of currency exchanged carries enormous implications.

For example, the value minted on the face of a one-ounce U.S. gold coin (Gold Eagle and Gold Buffalo) is fifty ($50) dollars. So a Gold Dollar is 1/50th of a one troy ounce legal tender gold coin. The exchange rate between paper and gold dollars varies, but has recently averaged around $20 to $30 paper dollars for $1 gold dollar. A Gold Cent is a hundredth of that amount.

When the medium of exchange is separated from the forces affecting property values, huge distortions can occur, leading to phantom appreciation, phantom tax burdens, and a phantom sense of financial security. Citizens can elect whatever form of legal tender they would like to use to establish their basis in capital assets, but because of the value separation that occurred during the mintage moratorium, it has never been practicable for ordinary citizens to handle the thousands of coins needed to stay on a specie legal tender platform, leaving them exposed to taxes not based on actual capital appreciation but currency-driven inflation.

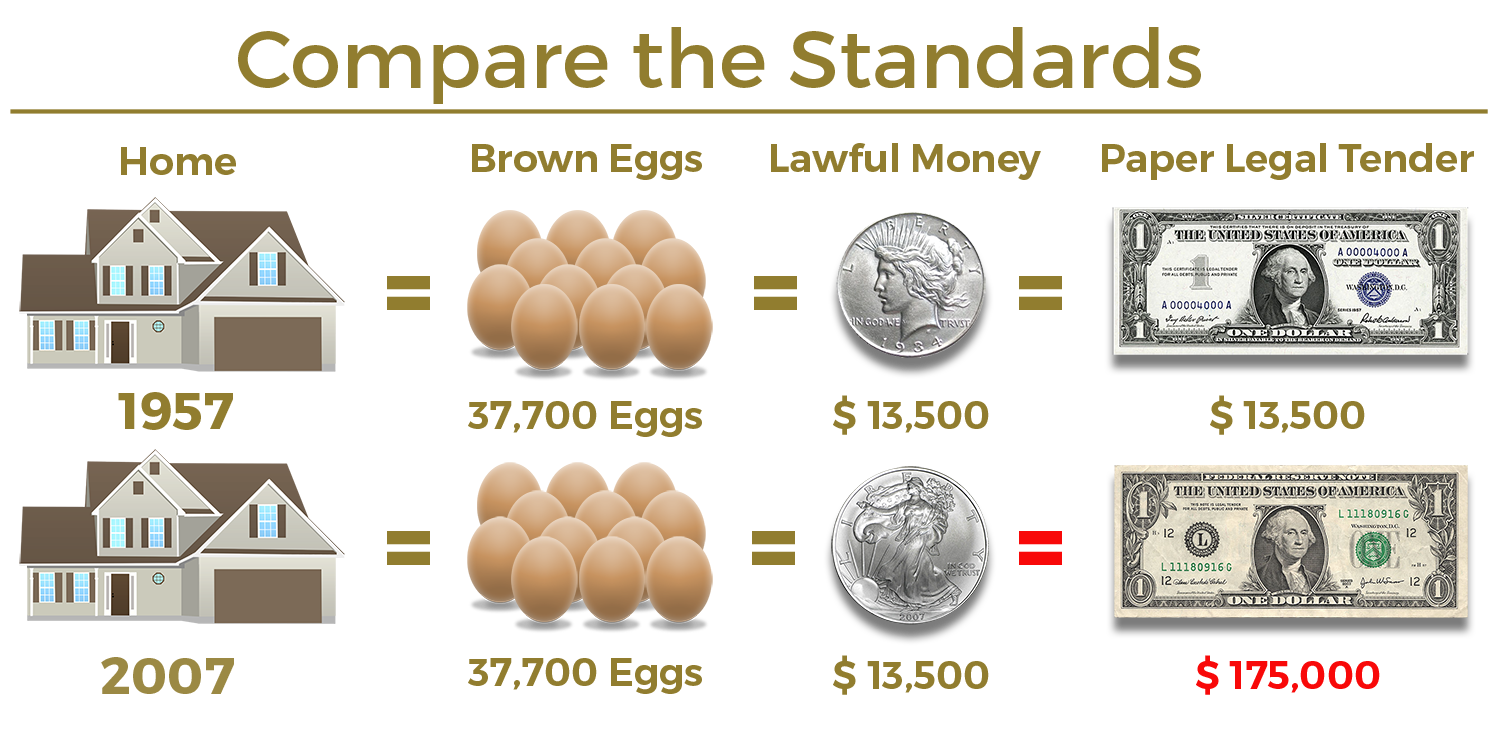

For example, the taxable gain on a rental house purchased in 1957 for $13,500 and sold in 2007 (fifty years later) would have been $0 under a silver dollar standard, because the purchasing power of a real silver dollar kept parity with the house value. Interestingly, gain on the sale of the house measured in brown eggs would be $0 as well,21 again because these values kept their parity. However, measured against the silver-backed paper dollar in 1957, the 2007 paper dollar did not keep parity with any of the other items and a sale transaction in paper currency would yield a paper-gain of $161,500. This underscores the effect of what some call the “inflation tax”, which noted economist John Maynard Keynes boasted “not one man in a million” could detect.22

The Quintric system helps manage phantom inflationary influences and distortions. For similar reasons, and because precious metals find their price stability on a global level, rather than national, the system can help manage foreign exchange (“forex”) exposure in a way heretofore not readily available, including cost reductions in administration and overhead related to treasury functions, hedging transaction costs, etc. Because of the advantages in managing forex exposure, the Quintric system could become very popular among multinational businesses with significant cross-border money flows, including repatriation.

While the federal government has expressly withdrawn its consent to obligations requiring tender of a particular type of dollar (31 U.S.C. § 5118), (meaning that a holder of the $50 gold certificate—as in the illustration above—can no longer demand a $50 gold coin from the U.S. Treasury), since 1977, private parties contracting under U.S. law are not prohibited from designating the form of legal tender in transactions between them, even though they still cannot require the U.S. Government to use a “gold clause” in a contract requiring the government to pay in gold. For private party transactions, the introduction of the Quint eliminates practical barriers to designating payments in specie legal tender. This makes the beneficial use of gold clauses feasible for employment contracts, capital asset purchases, long-term loan agreements, and in a myriad of other contexts.

D. Reduces the National Debt

When asked why the Reagan Administration had worked so tirelessly to reinstate precious metal coin as legal tender options for the American people, Then Secretary of the Treasury, Donald Regan, simply replied "to reduce the national debt."23 Indeed, that landmark legislation expressly provides:

Amounts received from the sale of gold shall be deposited by the Secretary in the general fund of the Treasury and shall be used for the sole purpose of reducing the national debt.24

The law also requires that the U.S. Secretary of the Treasury is to produce enough silver and gold American Eagles "sufficient to meet public demand."25 Thus, Reagan's legacy was to place firmly in the hands of the people an effective tool for federal debt reduction. That leaves a restoration of true choice in currency up to each American to do their part in electing to exchange paper dollars for gold ones and then to use them for the purchase of goods and services.